Merchant Services Explained: How Credit Card Processing Actually Works

While technical mastery of payment processing isn’t required to open your doors, a solid grasp of the mechanics empowers you to choose more efficient tools. This guide cuts through the noise to help you identify the best merchant services provider for your operations. How Credit Card Processing Works is a critical topic for businesses that want secure, fast, and reliable payment solutions. Understanding how credit card processing works helps business owners reduce transaction fees, improve customer experiences, and choose the right merchant services provider for their business needs.

Understanding Credit Card Processing

The journey of a card payment involves much more than a simple interaction at the register. While funds might appear in a business account within 24 to 48 hours—or even immediately for an extra charge—the interval between the initial tap and the final deposit is managed by a network of diverse intermediaries. Service providers like Patel Processing orchestrate this sequence, ensuring each participant completes their specific role. Learning this background is vital for entrepreneurs to pinpoint the origin of transaction costs and select a payment processor that aligns with their financial goals.

In the simplest terms, merchant services are the technology that enables a merchant to accept everything from standard credit and debit cards to digital gift cards and loyalty points. Gone are the days of clunky, universal systems that took forever to verify a sale. Modern processing is fast and highly customizable, offering specialized tools that fit the specific needs of different industries, making the checkout experience smoother for everyone involved.

Think about the different ways people buy. An eCommerce merchant needs credit card processing that integrates with a website’s shopping cart, offering ‘one-click’ checkouts and digital wallet options like Apple Pay to prevent people from abandoning their carts. A traditional retailer, however, needs a system that talks to their in-store inventory and can print or email a receipt right there on the spot.

The variety of payment tools available today is a huge benefit. It means you don’t have to settle for a generic tool that doesn’t fit your workflow. Since the technical side of things can be overwhelming, the smartest move is to connect with a reputable service provider. They can simplify the transition by helping you choose the right Point of Sale (POS) setup and training you on the best practices for payment processing for businesses.

How Merchant Services Work?

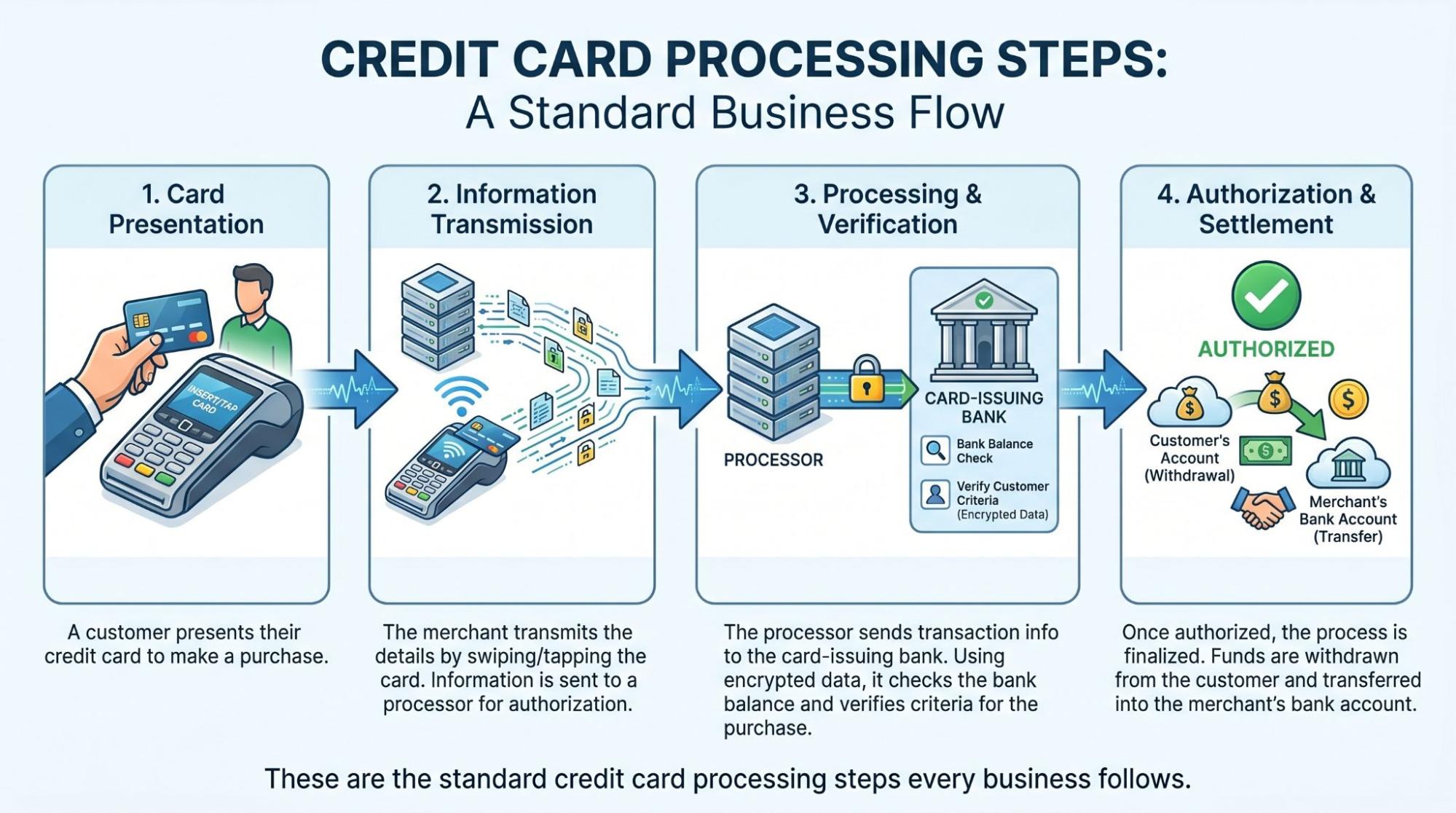

Most businesses today couldn’t survive without card payments. It’s essentially a high-speed data exchange where systems capture transaction info to authorize, clear, and settle every sale. To understand how merchant services work, you first need to see the logic: the bank that issued the card checks if the customer has enough money. Then, the processor grabs that data (even for virtual cards) and gets the wheels turning. Finally, during “settlement,” the actual money is moved into your bank account. To get started, you’ll need a merchant account and a bank you trust, plus a POS terminal or software to read the cards. While you can often sign up for these tools for free online, keep in mind that processors make their money through monthly service fees and a cut of every transaction.

What are merchant services in simple terms?

To put it simply it is the essential link that connects a shopper’s bank account to a business’s bank account. It handles the behind-the-scenes communication required to approve, verify, and complete every non-cash sale.

While it’s true that customers generally don’t pay a fee to use their cards, the service isn’t free. Merchants cover the operational costs through small fees—like interchange and markup fees—which fund the secure technology required to move money safely.

When it comes to shopping, for most people security is top priority. This makes merchants rely on processors that protect your information as it moves through the web. These services don’t just deal with the money, they are the backend that manages all the records and compliance rules required to accept cards. For the merchant, it’s a win-win because the service usually comes with ‘smart’ features that keep an eye out for suspicious activity and make it easier to stay in touch with their regulars.

Why Modern Credit Card Processing is a Game Changer for Your Income?

Give customers their preferred way to pay, and they will spend more. Research suggests that businesses can double or even triple their volume just by accepting cards. In fact, a significant 83% of entrepreneurs saw their numbers climb the moment they moved beyond cash. For 52% of those businesses, that meant at least an extra $12,000 in annual profit. At the top end, 18% of businesses saw a massive surge of $20,000 in new monthly sales. If you want to keep pace with your competitors, a solid payment setup is your best tool.

How many parties are involved in every Card Swipe?

Credit card processing is a service that helps businesses accept payments. It allows customers to pay with plastic cards or digital wallets. This process works because of three main groups: the merchant, the customer, and the processing company.

Different Businesses, Different Methods

Even though cards are common, not every business uses them the same way:

Small and Local Shops: For these owners, card processing is vital. Very few people carry cash today. These shops need processing services to make sales and stay in business.

Large Retailers: Giant companies like Walmart or Target often have their own methods. They deal with huge amounts of money. They might pay their bills with cash or use a system called Electronic Data Interchange (EDI). This system lets their computers talk directly to their suppliers.

For most businesses, the processing service is the middleman. It takes a customer’s card swipe and turns it into real money in the store’s bank account. Without it, most modern shops could not function.

Most card systems are run by banks or expert firms called merchant service providers. To get started, a business hires an ‘acquirer’ or ‘merchant processor’ to handle the technical side of every sale. These processors can be standalone companies or major banks that have permission to accept specific card brands. Because many of these providers are full-scale financial institutions, they often help with more than just payments—offering everything from business loans and insurance to smart tech tools that help a business owner track their daily cash flow.

Secure and Simple Credit Card Processing with Patel Processing

The technology you use at the checkout counter can actually help your business perform better. At Patel Processing, we specialize in payment solutions that make it easy to accept credit cards, debit cards, and phone-based payments both in-store and through your website. Our suite of merchant tools for small and large merchants is built to be innovative yet simple to use. We believe that processing a payment should be about more than just moving money—it should be about providing a secure, high-value experience for you and your customers alike.

Conclusion

Selecting the right payment processor is one of the most critical decisions an entrepreneur can make. By understanding how merchant services work, you move from simply “accepting payments” to strategically managing your cash flow and customer experience. Whether you are a small local shop or a growing eCommerce brand, the goal remains the same: provide a secure, seamless checkout that encourages repeat business. With a partner like Patel Processing, you can leverage these technical steps into a competitive advantage that drives real profit.

FAQs

1. How exactly does merchant credit card processing work?

Merchant credit card processing is a high-speed relay between four key players: your business, the payment processor, the card network (like Visa or Mastercard), and the customer’s bank. When a card is swiped, the processor asks the bank if funds are available. Once approved, the processor “clears” the transaction and eventually “settles” the funds by depositing them into your merchant account, usually within 24 to 48 hours.

2. How does credit card transaction processing work for online vs. in-person sales?

While the backend steps are similar, the “entry point” differs. In-person sales use a physical POS terminal to read the card’s chip or NFC signal. Online sales use a payment gateway, which acts as a virtual terminal to encrypt data entered on a website. Because the card isn’t physically present online, these “Card-Not-Present” (CNP) transactions often carry higher fees due to the increased risk of fraud.

3. Who pays the 3% credit card fee?

The merchant (the business owner) typically pays the processing fee. For a $100 sale, a 3% fee means the merchant receives $97, while $3 is split between the card-issuing bank, the card network, and the payment processor. In some regions, businesses are allowed to add a “surcharge” to pass this cost to the customer, but this is subject to strict local laws and card network rules.

4. Is a 3% transaction fee considered high in 2026?

In 2026, a 3% fee is generally considered on the higher end for standard in-person “swipe” transactions, which typically range from 1.5% to 2.5%. However, for eCommerce, international cards, or premium reward cards (like travel cards), 3% or even higher is quite common. To get the best merchant services provider rates, businesses often look for “Interchange-Plus” pricing rather than flat-rate pricing.

5. What are the 4 main types of credit card processing fees?

Interchange Fees: Paid to the customer’s bank (the largest portion).

Assessment Fees: Paid directly to the card network (Visa, Mastercard, etc.).

Processor Markup: The fee your service provider charges for their tools and support.

Incidentals: Fees for specific actions, like chargebacks, monthly minimums, or PCI compliance.

6. Can I get my money faster than the standard 48-hour settlement?

Yes. Many modern providers now offer Same-Day Funding or Instant Payouts. While standard settlement is usually included in your base rate, instant payouts often cost an additional 1% to 1.5% fee to move the money to your bank account within minutes.

7. What is the standard rule for merchants accepting credit cards?

The cardinal rule for merchants is to always prioritize security over speed. While a faster checkout is tempting, ensuring your business is PCI compliant and utilizing tools like EMV chip readers and 3D Secure is vital. Cutting corners may save seconds, but a single data breach or a surge in chargebacks can lead to heavy fines, reputation damage, or the loss of your merchant account entirely.